Bovenstaande creatieve montage geeft toch een goed beeld van de werkelijkheid. Voor de internationale financiële wereld is het nog steeds 'niet genoeg'. Alle bonzen in de geldwereld spelen mekaar de zwartepiet toe in de Commissie De Wit. Ja, ze hadden wel een kleinigheidje anders moeten doen, maar dan waren daar de wetten, was daar hun gebrek aan informatie, etc. Blijkbaar zijn er ook geheime afspraken waardoor Wellink ons bepaalde gegevens niet kan doorspelen. Zeker is dat er niet alleen fouten zijn gemaakt, maar dat ons hele financiële systeem rot is tot op het bot en op de schop moet. Daar ligt het hoofdprobleem. Er is niet zoveel misgegaan, de doelstellingen waren verkeerd van begin af aan. Het graaien was onderdeel van 'onze' financiële welvaart (voor sommigen dan).

Het erge is dat er waarschijnlijk helemaal niets gedaan zal worden om het systeem om te buigen. Nederland, en heel Europa, loopt aan de leiband van de VS. In de VS hebben een aantal criminele banken onverantwoorde risico's genomen, die doorverkocht werden en waarmee de hele wereld werd opgezadeld. Dat creëerde in een aantal landen een papieren bubbel, een balans op papier die er goed uitzag, maar het waren de nieuwe kleren van de keizer.

Het gevolg was dat regeringen overal moesten bijspringen om falende banken en instellingen te redden. Daarvoor moesten deze regeringen geld lenen en hun eigen land zodoende opzadelen met een gigantische schuld. Wouter Bos heeft zelfs een groot bedrag aan deposito's van Nederlanders in IJsland op voorschot uitbetaald terwijl niet eens zeker was dat hij dat geld terug zou krijgen. Dat was heel stom en niet fair tegenover de belastingbetaler. Waarom zou een oppassende burger solidair moeten zijn met de calculerende spaarder die zijn geld liever in het buitenland deponeert? Nu zitten wij met een groot risico.

Lees hoe de graaiers in de bankwereld nog steeds te werk gaan:

Crain's: "What should have been a profitable quarter a Lazard Ltd. turned into a surprising loss due to the investment bank paying its people big bonuses.

The firm doled out $616 million in compensation and benefits to about 2,300 employees last quarter, or more than triple the amount handed out in the same period in 2008. It was a consequence, Lazard said, of a decision to pay more bonuses in cash and accelerate some deferred cash awards from a prior year. But so great was the firm's generosity that compensation costs overwhelmed quarterly revenues and resulted in a net loss of about $55 million for the fourth quarter. The charges also almost wiped out full-year profits."

Wouter Bos heeft zijn reddingsmiljarden op de 'kapitaalmarkt' geleend. Wat ik graag zou willen weten is welke banken? De Nederlandsche Bank, ECB of andere banken? Waarom maakt Bos zelf geen geld ter financiering? Dat is toch het voorrecht van een staat of centrale bank, of in dit geval de Europese Centrale Bank? Het geleende geld behoort in feite ook tot de categorie van fictief geld waarvan maar hoogstens 10% reële waarde in echte deposito's aanwezig is. Heeft Bos misschien geld geleend van de VS? Dan zijn we het schip in. Dan zijn we afhankelijk van de grillen van de VS. Als het mis gaat met IJsland dan zitten we met een strop. Is het fair dat alle belastingbetalers in IJsland moeten betalen voor het graaien van een paar banken? Is het fair dat alle Nederlandse belastingbetalers moet opdraaien voor een risico veroorzaakt door calculerende burgers?

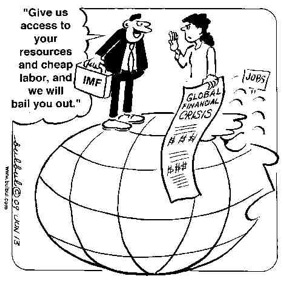

Dat de VS de oorzaak is van deze wereldcrisis is duidelijk. Sommige banken hebben doelbewust zichzelf verrijkt ten koste van anderen. Overheersing van de geldmarkt is een doel dat niet ontkend kan worden. Het IMF en de Wereldbank gaan over lijken. Dat is een feit. Is Europa nu ook het doelwit geworden? Het is zeer wel mogelijk. Daarom moet Europa een eigen koers gaan volgen. Dat is een bittere noodzaak. Verscheidene Europese staten zijn in problemen geraakt en staan op de rand van een failliet. Europa onder de knoet van het IMF zou een ramp zijn.

WebOfDebt: "Europe’s small, debt-strapped countries could follow the lead of Argentina and simply walk away from their debts. That would shift the burden to the creditor countries, which could solve the problem merely by a change in accounting rules.

Total financial collapse, once a problem only for developing countries, has now come to Europe. The International Monetary Fund is imposing its “austerity measures” on the outer circle of the European Union, with Greece, Iceland and Latvia the hardest hit. But these are not your ordinary third world debtor supplicants. If anyone can stand up to the IMF, these stalwart European warriors can.

And Iceland and Latvia have been saddled with responsibility for private obligations to which they were not parties. Economist Michael Hudson writes:

“The European Union and International Monetary Fund have told them to replace private debts with public obligations, and to pay by raising taxes, slashing public spending and obliging citizens to deplete their savings. Resentment is growing not only toward those who ran up these debts . . . but also toward the neoliberal foreign advisors and creditors who pressured these governments to sell off the banks and public infrastructure to insiders.”

Greece may be the first in the EU outer circle to revolt.

The currency cannot be devalued because the same Euro is used by all. That means that while the country’s ability to repay is being crippled by austerity measures, there is no way to lower the cost of the debt. Evans-Pritchard concludes:

“The deeper truth that few in Euroland are willing to discuss is that EMU is inherently dysfunctional – for Greece, for Germany, for everybody.”

Which is all the more reason that Iceland, which is not yet an EU member, might want to reconsider its position. As a condition of membership, Iceland is being required to endorse an agreement in which it would reimburse Dutch and British depositors who lost money in the collapse of IceSave, an offshore division of Iceland’s leading private bank. Eva Joly, a Norwegian-French magistrate hired to investigate the Icelandic bank collapse, calls it blackmail. She warns that succumbing to the EU’s demands will drain Iceland of its resources and its people, who are being forced to emigrate to find work.

Latvia is a member of the EU and is expected to adopt the Euro, but it has not yet reached that stage.

In November, the Latvian government adopted its harshest budget of recent years, with cuts of nearly 11%. The government had already raised taxes, slashed public spending and government wages, and shut dozens of schools and hospitals. As a result, the national bank forecasts a 17.5% decline in the economy this year, just when it needs a productive economy to get back on its feet. In Iceland, the economy contracted by 7.2% during the third quarter, the biggest fall on record. As in other countries squeezed by neo-liberal tourniquets on productivity, employment and output are being crippled, bringing these economies to their knees.

In November, the Latvian government adopted its harshest budget of recent years, with cuts of nearly 11%. The government had already raised taxes, slashed public spending and government wages, and shut dozens of schools and hospitals. As a result, the national bank forecasts a 17.5% decline in the economy this year, just when it needs a productive economy to get back on its feet. In Iceland, the economy contracted by 7.2% during the third quarter, the biggest fall on record. As in other countries squeezed by neo-liberal tourniquets on productivity, employment and output are being crippled, bringing these economies to their knees.

The cynical view is that that may have been the intent. Instead of helping post-Soviet nations develop self-reliant economies, writes Marshall Auerback, “the West has viewed them as economic oysters to be broken up to indebt them in order to extract interest charges and capital gains, leaving them empty shells.”

Iceland, Latvia and Greece are all in a position to call the bluff of the IMF and EU. In an October 1 article called “Latvia – the Insanity Continues,” Marshall Auerback maintained that Latvia’s debt problem could be fixed over a weekend, by a list of measures including (1) not answering the phone when foreign creditors call the government; (2) declaring the banks insolvent, converting their external debt to equity, and having them reopen with full deposit insurance guaranteed in local currency; and (3) offering “a local currency minimum wage job that includes healthcare to anyone willing and able to work as was done in Argentina after the Kirchner regime repudiated the IMF’s toxic package of debt repayment.”

Evans-Pritchard suggested a similar remedy for Greece, which he said could break out of its death loop by following the lead of Argentina. It could “restore its currency, devalue, pass a law switching internal euro debt into [the local currency], and ‘restructure’ foreign contracts.”

Standing up to the IMF is not a well-worn path, but Argentina forged the trail. In the face of dire predictions that the economy would collapse without foreign credit, in 2001 it defied its creditors and simply walked away from its debts. By the fall of 2004, three years after a record default on a debt of more than $100 billion, the country was well on the road to recovery; and it achieved this feat without foreign help.

Issuing and lending currency is the sovereign right of governments, and it is a right that Iceland will lose if it joins the EU, which forbids member states to borrow from their own central banks. Still, the people of these crisis-struck countries could continue to develop their own resources if they had the credit to do it; and with sovereign control over their local currencies, they could get that credit simply by creating it on the books of their own publicly-owned local banks.

Issuing and lending currency is the sovereign right of governments, and it is a right that Iceland will lose if it joins the EU, which forbids member states to borrow from their own central banks. Still, the people of these crisis-struck countries could continue to develop their own resources if they had the credit to do it; and with sovereign control over their local currencies, they could get that credit simply by creating it on the books of their own publicly-owned local banks.

In fact, there is nothing extraordinary in that proposal. All private banks get the credit they lend simply by creating it on their books. Contrary to popular belief, banks do not lend their own money or their depositors’ money. As the U.S. Federal Reserve attests, banks lend new money, created by double-entry bookkeeping as a deposit of the borrower on one side of the bank’s books and as an asset of the bank on the other.

Besides thawing frozen credit pipes, credit created by governments has the advantage that it can be issued interest-free. Eliminating the cost of interest can cut production costs dramatically.

When the debtor nation refuses to pay, the burden shifts to the creditors to make themselves whole. British economist Michael Rowbotham suggests that in the modern world of electronic money, this can be accomplished by creative banking regulators simply with a change in accounting rules. “Debt” today is created with accounting entries, and it can be reversed with accounting entries. Rowbotham outlines two ways the rules might be changed to liquidate impossible-to-repay debt:

“The first option is to remove the obligation on banks to maintain parity between assets and liabilities . . . . Thus, if a commercial bank held $10 billion worth of developing country debt bonds, after cancellation it would be permitted in perpetuity to have a $10 billion dollar deficit in its assets. This is a simple matter of record-keeping.

“The second option . . . is to cancel the debt bonds, yet permit banks to retain them for purposes of accountancy. The debts would be cancelled so far as the developing nations were concerned, but still valid for the purposes of a bank’s accounts. The bonds would then be held as permanent, non-negotiable assets, at face value.”

If the banks were allowed either to carry unrepayable loans on their books or to accept payment in local currency, their assets and their solvency would be preserved. Everyone could shake hands and get back to work."

Parakalo: "De economische crisis treft ook Griekenland in alle hevigheid. De Europese Commissie waarschuwt voor een lange periode zonder economische groei en een stijging van de werkloosheid met meer dan tien procent. In werkelijkheid zal het aantal mensen zonder baan nog veel sterker toenemen omdat veel migranten in Griekenland werkzaam zijn in het grijze circuit en dus niet worden meegenomen in de voorspellingen."

CurrentConcerns: "But what will happen, if the initially specified prognoses on the coming national debts will come true? How will those responsible in the EU and in the states react? Will more and more EU states have to explain their financial bankruptcy? Will more and more EU states be downgraded by the rating agencies in their creditworthiness due to their high debts – as has already happened in some cases – and then charged with even higher interest rates by the financiers? Will the powerful states in the EU put even more pressure on those states with little influence so that they have to submit to the financial interests of the larger ones and mutate even further toward a “directorate of the big ones and some of their vassals” (Jean Asselborn)? Will the EU become an increasingly blatant instrument of redistribution in favor of the high finance? Will increasingly sumptuous interest payments to the financiers eventually replace the actual state operations? Will more national services be privatized – so that public interest becomes an even smaller and profit an even bigger criterion for state expenditures? Or will the governments of the EU member states try their luck with a value-destroying inflationist policy?"

Indien de VS Europa in een houdgreep blijft houden dan zou de druk vanuit Europa op Griekenland om 'orde op zaken te stellen' (vreemd want de orde is verstoord door de VS) dan zou de Euro in kunnen storten. De vraag is of Europa bereid en in staat is zich financieel los te maken van de VS. Dat is wat de realiteit nu toch eist. Het is de enige oplossing. Het doel van het IMF is het scheppen en in stand houden van schulden over de hele wereld. Het is een instrument van overheersing. De degradatie van Europa tot de status van derdewereldland is ondenkbaar en zou tot revolutie leiden. De enige oplossing is het afboeken van de nationale schuldenlast. De schuldenlast is sowieso al onrechtvaardig, want gebaseerd op het doelbewust financieel onderdrukken van landen met verschrikkelijke gevolgen voor de inwoners. Schulden zijn voor het grootste deel ficties, net als het scheppen van geld door de banken een fictie is.